As a CERTIFIED FINANCIAL PLANNER®, my greatest motivation is to help my clients reach their goals. When starting a new relationship, we make it clear that financial planning and wealth management strategies are not just about achieving numerical goals, but about how those numerical goals will help you realize your lifestyle and life’s worth goals.

Below, I share a hypothetical story about two fictional clients: Marty and Jennifer. I’m sharing this story in the hope that as you read about this financial situation and the vision these hypothetical clients have for their future, you’ll be inspired to take the steps needed to begin working toward your own goals. As you read this story, you will gain an understanding of how I typically work with my clients to design custom strategies in pursuit of success.

It’s never too late to start saving for retirement or working toward another financial milestone. But the sooner you take action, the easier it will be to achieve the goals you have for your future.

Background

Marty and Jennifer are in their early 40s. They are a married couple with three young children aged 7, 11, and 13. Marty is a key employee with an ownership stake in a small business that was recently acquired by a private equity firm. Jennifer is a registered nurse at a private clinic in their community.

The couple earns a combined annual income of $500,000. As part of the buyout of the small business, Marty is receiving a cash payout of $900,000 plus stock in the new company. Marty and Jennifer each maximize their contributions to employer-sponsored 401(k) plans. Marty participates in a Roth 401(k) with a balance of $20,000 and Jennifer participates in a traditional 401(k) with a balance of $50,000. They have $200,000 in savings, but no other investments.

Their expenses are around $217,000 each year. Part of these expenses includes two mortgages they have on the home they purchased in 2020. The first is a traditional 30-year mortgage at $500,000. The second, at $145,000, is a 15-year mortgage with a balloon payment at year 15.

With their extra cash as well as the recent cash payout from the sale of Marty’s small business, the couple needs help knowing exactly what they could be doing to optimize their chances of reaching their financial and lifestyle goals for the future.

Marty & Jennifer’s Goals: Early Retirement & Beyond

One of Marty and Jennifer’s top priorities is that they will both be able to retire by age 55. Because they enjoy their current lifestyle, they want to be able to maintain their standard of living throughout their working and retirement years. They’d also like to have $100,000 set aside for each of their children’s college education for a total of $300,000.

They have two main questions in addition to the goals outlined above (you may find yourself with similar questions):

- Should they pay off their mortgage early or invest that extra cash in the markets?

- How could they anticipate, plan for, and possibly minimize the tax liability of Marty’s cash payout from the business sale?

Marty and Jennifer were maximizing their 401(k) contributions and are diligent savers, but they don’t have a current investment strategy or savings plan. Because of their ambitious goal to retire at 55, they need an investment strategy and savings plan as soon as possible. They also need to develop an estate plan with a will, power of attorney designation, and guardianship for their children if something were to happen to them.

Recommended Strategies

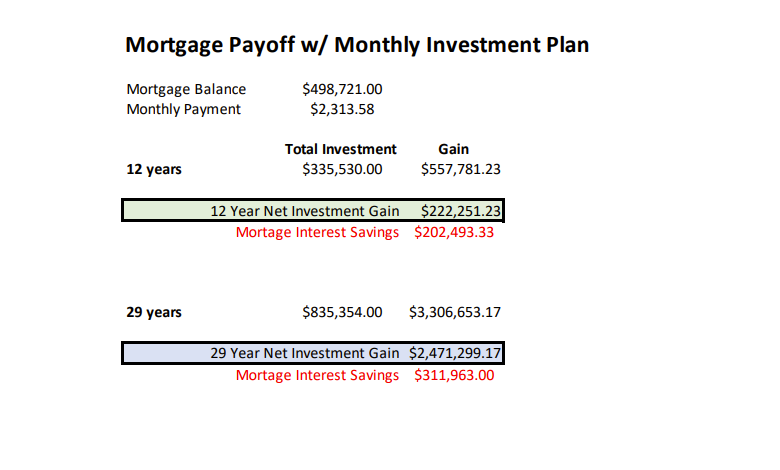

To begin, I would address their first question about whether to pay off their mortgage early or invest their cash in a brokerage account. I would help them analyze the opportunity cost of paying off the mortgage vs. investing in the markets, which you can see an example of below.

As you can see, paying off the mortgage early wouldn’t save a significant amount in interest costs compared to the exponential growth potential of investing that cash. However, because in this example, the 15-year mortgage has a higher interest rate and a balloon payment at the end of the term, I would recommend to pay off that mortgage and invest the remaining cash each month.

Additionally, I would help them create an investment plan for their remaining cash and review their 401(k) asset allocations. Based on the goal to retire at 55 (just over 10 years away in this example), it’s important that their assets are properly allocated to generate the necessary returns without positioning them for too much risk. Because this couple is relatively close to retirement, I would provide ongoing annual reviews to adjust their allocations if needed.

Finally, I would recommend they fund a 529 plan for each of their children with a beginning balance of $25,000. To reach their $100,000 goal for each, we would calculate the amount of the annual contributions they could make as well.

Actions & Anticipated Outcomes

We would also need to address the second concern regarding tax liabilities associated with Marty’s cash payout. To ensure that investment plans and strategies are aligned with their tax strategies, I would collaborate with their CPA to estimate the taxes due on the cash payout and plan for them to make quarterly estimated payments to reduce tax penalties during tax season.

I would then create an annual investment and savings plan consisting of actionable steps the couple could take to achieve each of the long-term goals: mortgage payoff, education savings, and early retirement.

Finally, Marty and Jennifer are at the point that they need to start thinking more seriously about their estate plans and life insurance protection. Because they have three young kids, they need to make certain that the kids and/or surviving spouse would be taken care of if the worst were to happen to one or both of them.

We would begin with the most important actions first and partner with an estate planning attorney to establish their will and guardianship documents to protect the kids. We would then evaluate their life insurance needs to ensure that if something happens to one or the other, the surviving spouse and minor children would be able to continue with their lives and plans for the future without suffering financial distress.

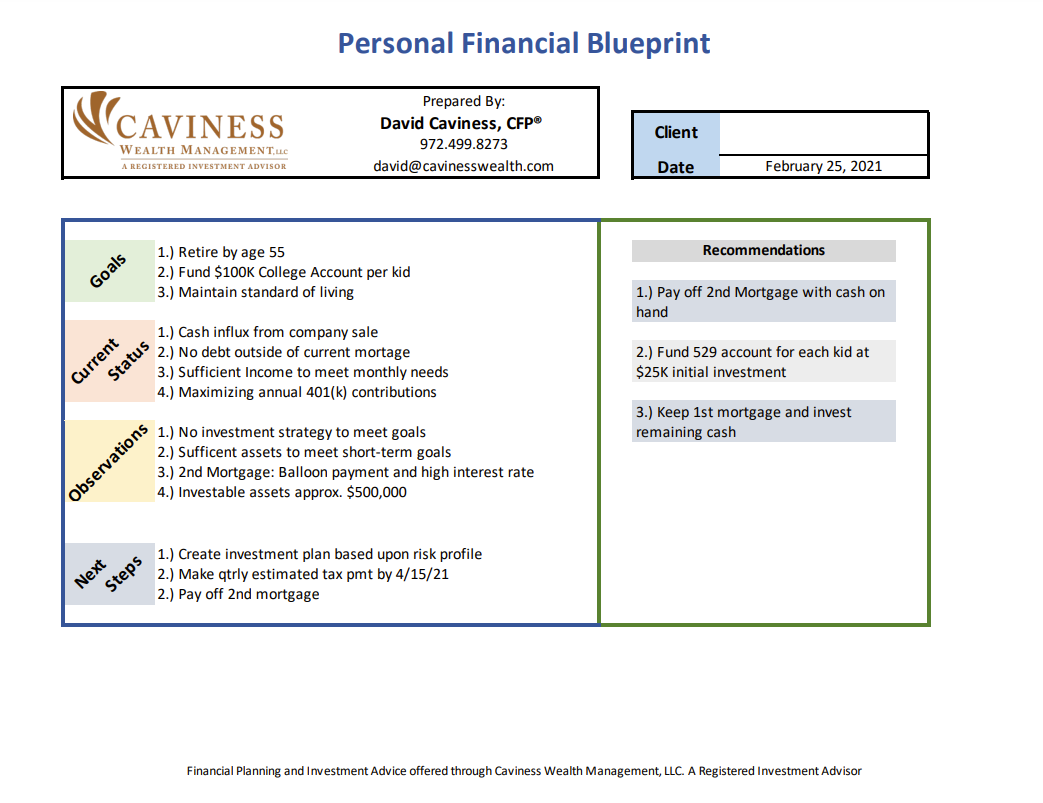

Below is a sample of Marty and Jennifer’s Personal Financial Blueprint. One of my priorities is to make financial planning and wealth management strategies as simplified as possible for my clients, so I always provide a one-page Blueprint that streamlines their most important decisions and outlines the goals those decisions will help them achieve.

Ultimately, based on the hypothetical background and earnings of these fictional characters, these are strategies I would implement with my own clients to help them increase their chances of success and plan for their ambitious goals. My hope for the remainder of this year is to help many more families achieve their unique financial goals by optimizing their resources and creating actionable plans that can be implemented today.

What Are Your Financial Goals & Challenges?

If you have ambitious financial goals, but aren’t sure about the best way to achieve them, it may be time to partner with a financial planner and wealth manager. You may be uncertain about the actions you need to take, or you may have a general idea but don’t know how to decide between two or more options.

Whatever your situation, I can help you discover and prioritize the steps you need to take for your future. If you have any doubts that are preventing you from taking action, it’s time to confront those doubts today. To see if I can help you using recommendations and strategies similar to the ones described above, click here to schedule a conversation with me.

Prior to investing in a 529 Plan investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing.

The content in this material is based on a hypothetical example used for illustrative purposes only and is not representative of any specific investment or recommendation.